Plenty of owners are told that electing S-corp status removes self-employment tax. They file an S election expecting to save the full 15.3%. At lower profit levels, most of it never shows up.

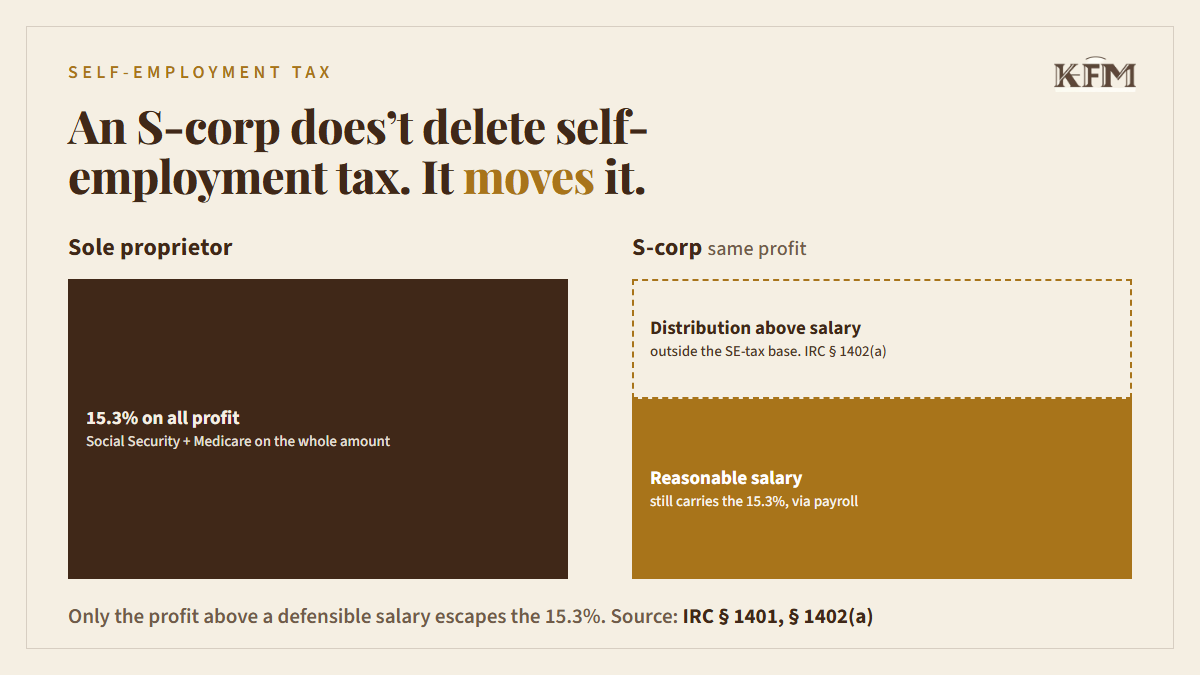

Self-employment tax is the Social Security and Medicare tax you pay on your own business profit when you work for yourself. A sole proprietor or partner pays it on all of their business income. The base rate is 15.3%: 12.4% for Social Security and 2.9% for Medicare. That is the number people are trying to escape, and the S-corp changes how it lands without removing it.

Self-employment tax is built on a defined base the law calls "net earnings from self-employment." That base is the income from a trade or business you carry on yourself, plus a partner's share of partnership income. The statute stops there. It never adds an S-corp shareholder's share of the company's profit. So when your business is an S-corp, the profit that passes through to your personal return is outside the self-employment tax base. That is the whole reason the election can save anything at all.

But the same law that lets the profit through requires something in return. If you work in your own S-corp, the IRS treats you as an employee, and you have to pay yourself a "reasonable salary," meaning wages for the work you actually do, before you take any profit as a distribution. Those wages run through payroll, and payroll carries the identical 15.3%: 6.2% Social Security and 1.45% Medicare from you, the same again from the company. The same load now lands on the salary line instead of the whole profit. The only money that escapes the 15.3% is the slice of profit you can defensibly take as a distribution above that salary.

That word "reasonable" is where the savings gets thin, and a court has already drawn the line. In Watson, an accountant paid himself a $24,000 salary out of a firm throwing off far more, and took the rest as distributions. The court held $24,000 was not a reasonable wage for his work and treated $91,044 as the salary that should have carried employment tax. The test is whether the money was really pay for services, and your wish to keep the salary low does not control the answer. The lower you set the salary to widen the tax-free distribution, the more of it the IRS can push back onto the wage line.

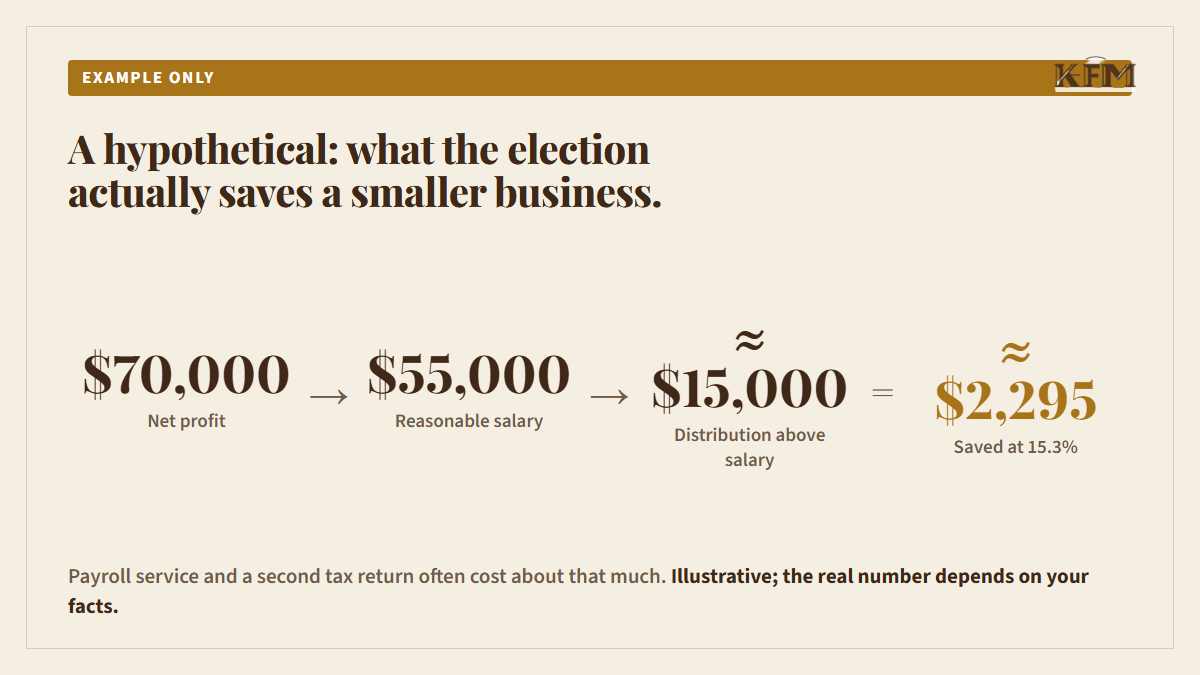

Run a smaller business through it. Say the company's net income is $70,000 and a defensible salary for the work is $55,000. The distribution you can safely take is about $15,000, and 15.3% of that is roughly $2,295, which is the entire saving. Against it sits payroll service, a separate corporate return, and the bookkeeping an S-corp demands, which together often run most or all of that $2,295. At lower profits the defensible salary eats almost the whole profit, the distribution shrinks toward zero, and the saving shrinks with it.

Two exceptions, both narrow. First, these are federal employment-tax figures; Florida has no personal income tax, so for Florida owners this is the whole calculation. Second, the Social Security half stops at a wage ceiling of $184,500 for 2026, while the Medicare half never stops, and an extra 0.9% applies above $200,000 of self-employment income (or, on the wage side, wages) for a single filer or $250,000 for a married couple. None of that changes the picture for an owner well under that ceiling.

An S-corp converts self-employment tax into payroll tax and only saves you the rate on whatever profit survives above a salary you could defend to the IRS. For a smaller business that margin is slim, so the election only pays off on the profit it actually frees up.

If you want to know whether your profit clears that line, reply with your entity type and rough net profit, and I'll tell you the first number I'd check.

Comments