"I'm going to form an LLC to save on taxes." Owners say it the way they'd say they're switching banks, as if registering the company by itself changes what they owe. It doesn't, and the rule that explains why has been settled for decades.

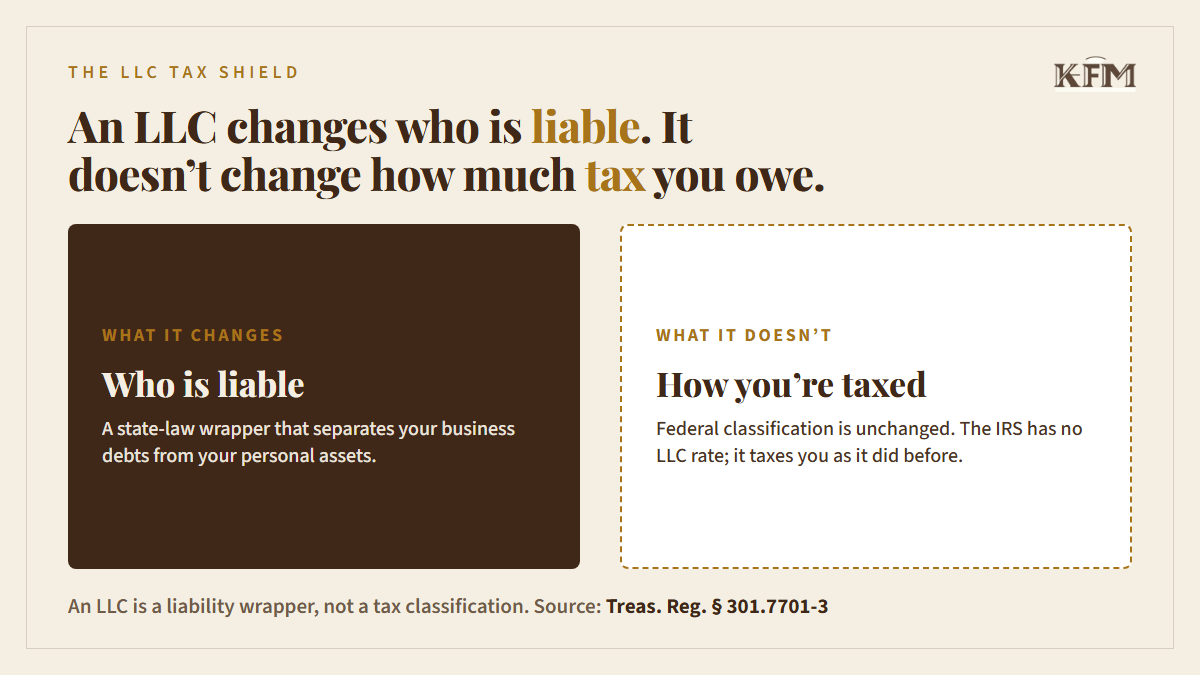

An LLC is a limited liability company. It is set up under state law, and it keeps your business debts separate from your personal money and property. That separation is real and often worth having. But "limited liability company" is not a line on a federal tax form. The IRS does not have an LLC tax rate. For federal income tax, an LLC is not its own kind of taxpayer at all.

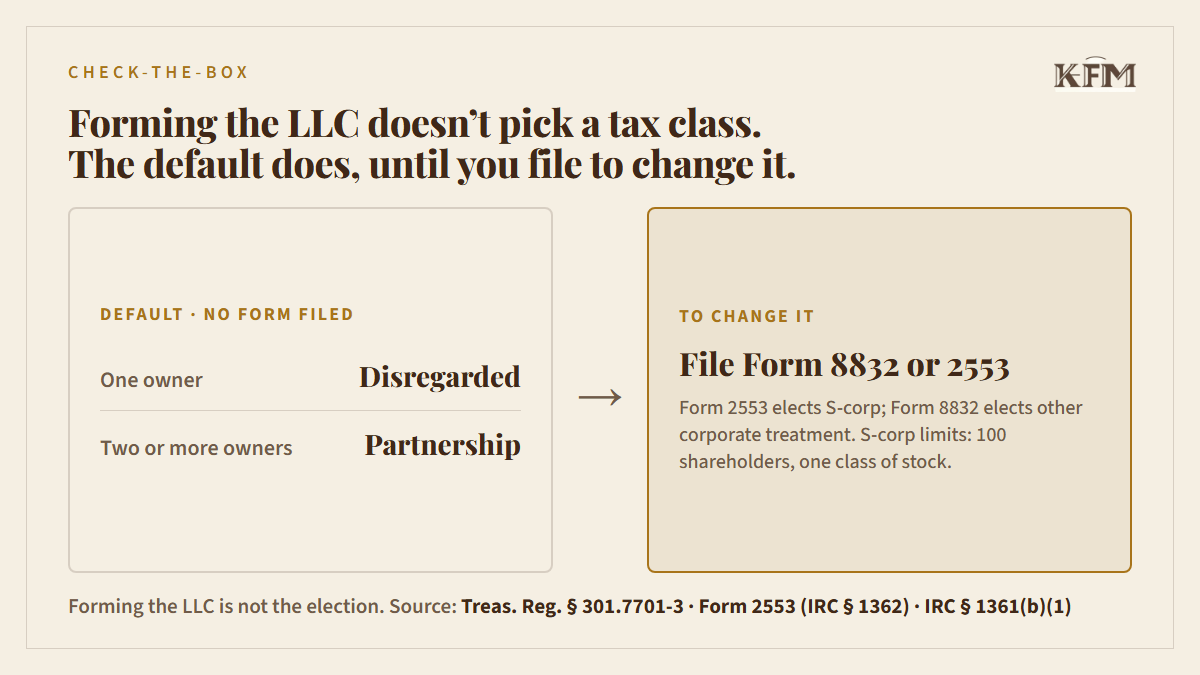

The rule that governs this is called check-the-box, and it has been settled since January 1, 1997 (Treas. Reg. § 301.7701-3, finalized by Treasury Decision 8697). It treats an LLC as an "eligible entity." That means the LLC does not arrive with a tax label of its own; it gets assigned one. The rule sets a default, then lets you change it. With no form filed, an LLC with two or more owners is taxed as a partnership. An LLC with one owner is "disregarded as an entity separate from its owner." Disregarded is the key word. For income tax, the IRS looks straight through the LLC and taxes the owner as if it weren't there.

Now compare how that same owner was taxed the day before they registered. A solo owner reports the business profit on their own return. After forming a single-member LLC, that owner is disregarded and still reports the profit on their own return. A two-person business taxed as a partnership before the LLC is taxed as a partnership after it. Either way the income passes through: the business pays no income tax itself, and the profit shows up on the owners' personal returns. The classification did not change, because registering the LLC is not the kind of step that changes it.

So where does the "tax savings" story come from? Usually from choosing to be taxed as an S corporation. That is a different tax treatment, and for some owners it can lower self-employment tax by splitting their pay into a salary and a separate payout. But it is a separate step you have to choose. You make it by filing Form 2553, the S-corporation election. An LLC that files Form 2553 on time is automatically treated as a corporation for tax purposes, so it does not also file Form 8832. (Form 8832 is the form for the other tax treatments, corporation, partnership, or disregarded, and it cannot elect S-corp status on its own.) Either way, the change comes from filing the form, not from the LLC. The S-corp route also has conditions. The business has to count as a "small business corporation," which the tax code limits to no more than 100 shareholders, owners who are only individuals or certain estates and trusts, no nonresident-alien owners, and a single class of stock (IRC § 1361(b)(1)). Whether it saves a given owner anything depends on their numbers and on paying a reasonable salary. It is not automatic.

The common advice runs two decisions together. Choosing the liability protection and choosing the tax treatment are separate choices, and the second one only happens if you go and make it.

For a Florida owner there is one more point worth adding. The whole "shield" framing is federal. Florida has no personal income tax, so there is no state income tax for an LLC to shield in the first place. The only income tax in play is the federal one, and the LLC did not change that.

So an LLC sets who is on the hook for the business debts. It does not set how much tax you owe. Changing the tax treatment is a separate choice, and it only happens when you file for it. If you are weighing whether your LLC should make that choice, reply with your owner count and rough profit, and I will tell you which option is worth pricing out.

Comments